Inflation is among the most important economic risks faced by individual investors. Following the outbreak of the COVID-19 pandemic and the war in Ukraine, inflation resurfaced in many countries. Because of this rising inflation and the increasingly important role individual investors play in capital markets, a growing number of articles in the financial press discuss how individual investors could preserve the real value of their financial wealth against rising prices, with many of them pointing toward investments in stocks.1 However, little is known about how individual investors actually respond to the prospect of higher inflation, and theory provides conflicting hypotheses on this issue. On the one hand, the hedging hypothesis predicts that investors are more likely to buy and less likely to sell stocks when expected inflation increases. This is because investors understand that stocks entitle them to a fraction of the income generated by the underlying real assets, allowing them to preserve the real value of their investments (e.g. Fama and Schwert 1977, Fama 1981, Boudoukh and Richardson 1993, Bekaert and Wang 2010). On the other hand, the money illusion hypothesis suggests that investors are less likely to buy and more likely to sell stocks in periods of higher expected inflation. This is because they adjust nominal interest rates but ignore that firms’ cash flows also grow with inflation, leading them to require higher dividend yields to hold stocks (e.g. Modigliani and Cohn 1979, Ritter and Warr 2002, Cohen et al. 2005). Given these two competing hypotheses, understanding how individual investors react to expected inflation is an empirical question.

Germany in the 1920s as a laboratory

A test of individual investors’ response to inflation is subject to three main empirical challenges. First, one needs granular data on investors’ security transactions. This allows for direct analysis of investment decision-making in inflationary periods. Second, one needs a period in which inflation, if overlooked, produces sizable financial losses and thus attracts the attention of investors.2 Third, one needs a reliable measure of expected inflation that varies both over time and across investors. This is a necessary condition for a within-person analysis and enables one to control for the overall time trend.

This setup is not available in the most common investor-level datasets. In a new study (Braggion et al. 2022), we introduce a unique dataset containing security portfolios of over 2,000 private clients of a German bank between 1920 and 1924, the period of the German hyperinflation. The data and the time are ideally suited to address each of the empirical challenges outlined above. First, we have detailed information on every trade executed by the bank’s clients, allowing for direct analysis of individuals’ investment behaviour. Second, inflation was high between January 1920 and September 1923, potentially yielding large financial losses if overlooked and arguably grabbing investors’ attention. Third, we have inflation data at a monthly frequency for hundreds of towns in Germany, resulting in an inflation measure that captures inflation experienced locally over time, which should be a reliable proxy for expected inflation.3

Individual investors buy less (sell more) stocks when facing higher inflation

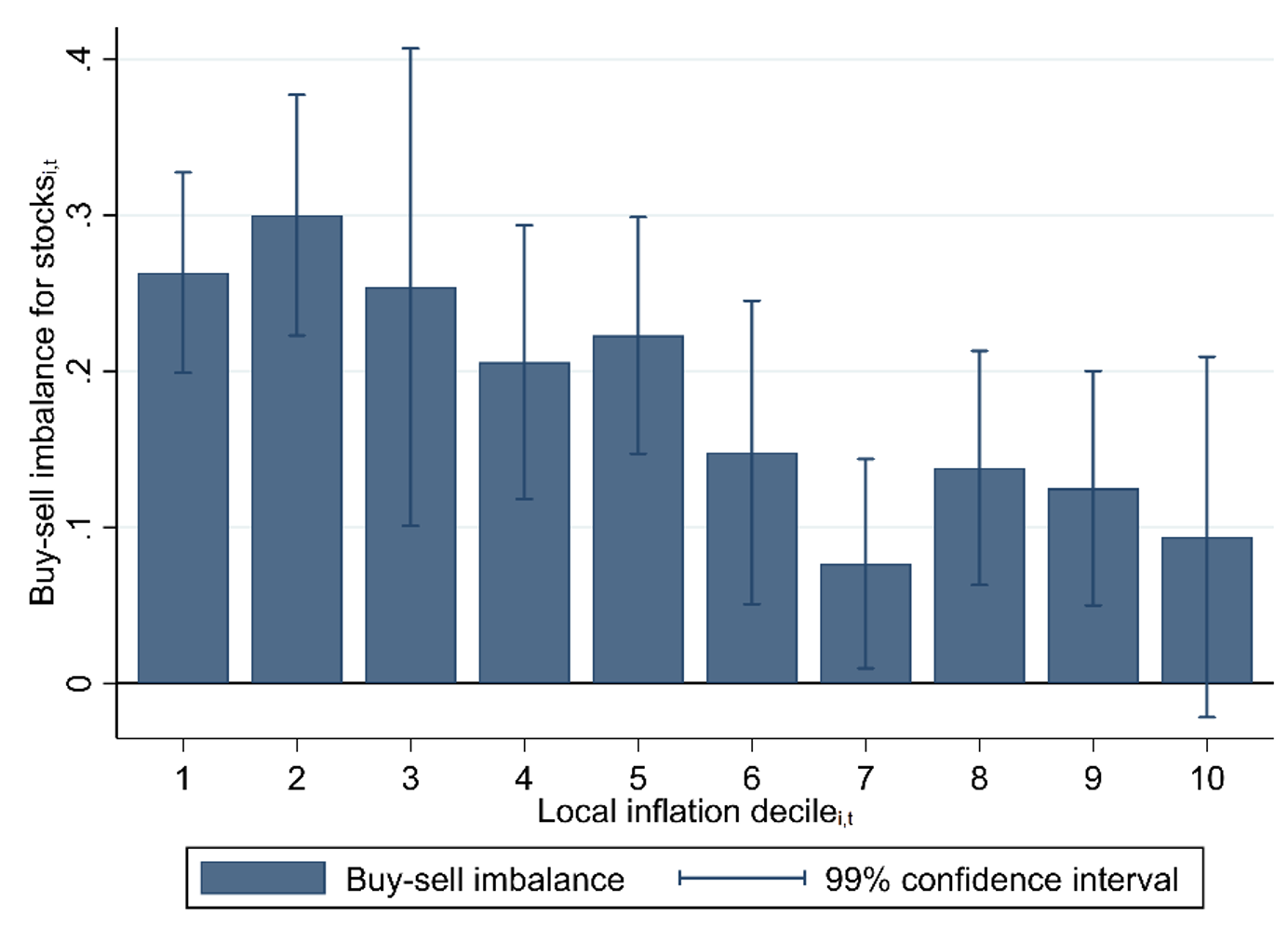

Figure 1 visualises our main finding. Each month, we sort towns in Germany into deciles based on their local inflation and compute, for each inflation decile, the average buy-sell imbalance for stock trades of clients living in those towns. The buy-sell imbalance captures individual investors’ net demand for stocks. We then plot average buy-sell imbalances against inflation deciles. The figure shows a strong negative relationship between the two. This suggests that investors buy less (sell more) stocks when facing higher local inflation. Moving from the decile with the lowest inflation to the decile with the highest inflation reduces buy-sell imbalances by 17 percentage points. More formal regression-based analyses confirm this result. Hence, we find investor behaviour consistent with the money illusion hypothesis but inconsistent with the hedging hypothesis.

Figure 1 Local inflation and stock trades

In additional tests, we find the negative relationship between local inflation and buy-sell imbalances for stocks to be attenuated for more sophisticated clients. For institutional clients of our bank, we even document a positive association between local inflation and buy-sell imbalances. These findings support the notion that sophistication reduces money illusion.

We also find a positive relationship between local inflation and foregone real returns following stock sales, suggesting that investors facing higher local inflation mistime their sales and incur extra losses. This evidence is again consistent with investors committing an inflation-induced investment mistake.

A large number of robustness tests indicate that our findings are unlikely to be driven by investors using local inflation as a proxy for future economic outcomes, by investors’ risk aversion increasing with local inflation, by investors liquidating stocks to meet consumption needs, and by investors shifting to other asset classes also offering a hedge against inflation.

Conclusion

Our analysis provides evidence that individual investors, in particular unsophisticated ones, make inflation-induced trading errors. This stresses the importance of the ongoing debate on the financial literacy of individuals. Recently, the European Commission pointed toward the limited financial literacy of households and advocated for making financial education a priority for Europe. Similar calls were made in the US.4 Our findings underscore concerns that the financial literacy of individuals may not be sufficient to respond appropriately to the currently resurfacing inflation.

References

Bekaert, G and X Wang (2010), “Inflation risk and the inflation risk premium”, Economic Policy 25(64) 755–806.

Boudoukh, J and M Richardson (1993), “Stock returns and inflation: A long-horizon perspective”, American Economic Review 83(5) 1346–1355.

Braggion, F, F von Meyerinck, and N Schaub (2022), “Inflation and individual investors’ behavior: Evidence from the German hyperinflation”, CEPR Discussion Paper No. DP15947.

Cohen, R B, C Polk, and T Vuolteenaho (2005), “Money illusion in the stock market: The Modigliani-Cohn hypothesis”, Quarterly Journal of Economics 120(2) 639–668.

D’Acunto, F, U Malmendier, J Ospina, and M Weber (2021), “Exposure to grocery prices and inflation expectations”, Journal of Political Economy 129(5) 1615–1639.

Fama, E F (1981), “Stock returns, real activity, inflation, and money”, American Economic Review 71(4) 545–565.

Fama, E F and G W Schwert (1977), “Asset returns and inflation”, Journal of Financial Economics 5(2) 115–146.

Katz, M, H Lustig, and L Larsen (2017), “Are stocks real assets? Sticky discount rates in stock markets”, Review of Financial Studies 30(2) 539–587.

Malmendier, U and S Nagel (2016), “Learning from inflation experiences”, Quarterly Journal of Economics 131(1) 53–87.

Mankiw, N G and R Reis (2002), “Sticky information versus sticky prices: A proposal to replace the new Keynesian Phillips curve”, Quarterly Journal of Economics 117(4) 1295–1328.

Modigliani, F and R A Cohn (1979), “Inflation, rational valuation and the market”, Financial Analyst Journal 35(2) 24–44.

Ritter, J R and R S Warr (2002), “The decline of inflation and the Bull Market of 1982-1999”, Journal of Financial and Quantitative Analysis 37(1) 29–61.

Sims, C A (2003), “Implications of rational inattention”, Journal of Monetary Economics 50(3) 665–690.

Endnotes

1 See, for example, “Inflation is coming. How much, for how long?”, New York Times, 6 June 2021; “Inflation poses a duration problem for investors”, Financial Times, 16 June 2021; “Inflation could mean value stocks’ time to shine”, Wall Street Journal, 26 October 2021; “Best investments to beat inflation”, Forbes, 28 December 2021; “Flight to ‘safe haven’ funds runs its own risk”, Financial Times, 7 March 2022; “Stocks as inflation hedge is new catch-all narrative for market rally”, Bloomberg, 22 March 2022.

2 In periods of low inflation, investors may not react to inflation because of rational inattention (e.g. Mankiw and Reis 2002, Sims 2003, Katz et al. 2017).

3 Existing empirical work shows that the inflation experienced personally is a crucial determinant of individuals’ inflation expectations (e.g. Malmendier and Nagel 2016, D’Acunto et al. 2021).

4 See, for example, “‘We need people to know the ABC of finance’: facing up to the financial literacy crisis”; Financial Times, 4 October 2021; “Education Secretary Miguel Cardona says personal finance lessons should start as early as possible”, CNBC, 13 October 2021; “Improving financial literacy must be a priority for Europe”, Financial Times, 17 January 2022.

from Stock Trading – My Blog https://ift.tt/7hvyz6T

via IFTTT

No comments:

Post a Comment